Introduction

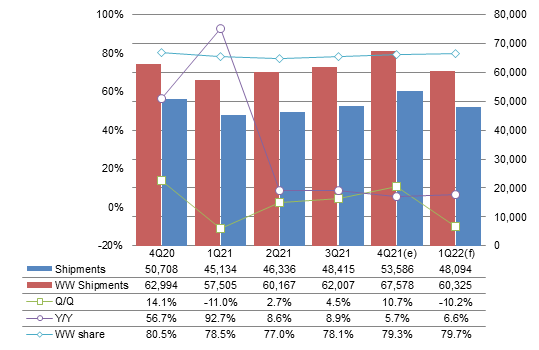

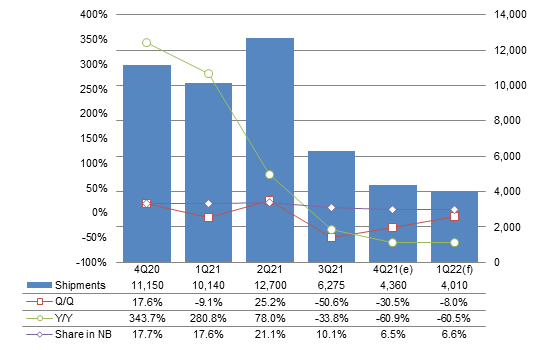

Chart 1: Notebook shipments, 4Q20-1Q22 (k units)

Source: Digitimes Research, January 2022

Taiwan's notebook shipments enjoyed better-than-expected growths in the fourth quarter of 2021, picking up over 10% sequentially, stronger than the 9% of the global average. The shipments increased 5.7% on year. (Note: Unless otherwise indicated, all figures and tables in this report refer to output from Taiwan makers.)

Despite Chromebooks' feeble demand, brand vendors' robust orders for enterprise notebooks that were mostly given to Taiwanese ODMs significantly drove up Taiwan's notebook output in the fourth quarter.

With a sequential shipment growth stronger than the global average, Taiwan's share in worldwide notebook shipments went up slightly by 1.2pp from a quarter ago to 79.3% in the fourth quarter.

Taiwan's shipments will plunge 10.2% sequentially in the first quarter of 2022, but will still be up by 6.6% on year.

Since the decline will also be smaller than the global average, Taiwan's share will rise further to 79.7%.

Notebooks powered by Intel's new Alder Lake platform will become available in the first quarter of 2022 and these new machines will mostly be assembled by Taiwanese ODMs.

(Note: Digitimes Research treats detachable notebook products as tablets. Convertible notebooks with undetachable keyboards are considered notebooks.)

Chart 2: Global notebook shipments, 4Q20-1Q22 (k units)

Source: Digitimes Research, January 2022

Global notebook shipments had a performance stronger than Digitimes Research anticipated in October, growing 9% sequentially and 7.3% on year to come to a new highest record ever, taking over the previous peak in the fourth quarter of 2020.

Major improvements in supply of battery- and panel-related ICs and the gradual restoration of the global logistic system and harbor congestion allowed brand vendors to significantly increase their shipments in the fourth quarter.

Hewlett-Packard (HP) and Lenovo saw their shipments soar in the fourth quarter of 2021 with increased supply of Full HD panels and power management ICs.

Notebook shipments are expected to plummet 10.7% sequentially in the first quarter of 2022, but the volumes will stay above 60 million units with an on-year growth of 4.9%.

The sequential decline in the first quarter of 2022 was a result of decelerated demand for notebooks in key markets worldwide.

Mature markets where the penetration of consumer notebooks is high are expected to face weak demand due to the first quarter of 2022 being the traditional slow season.

Because of component shortages, the enterprise segment in the first quarter of 2022 is still seeing some unsatisfied orders that were deferred from the previous quarter. However, the volumes of the deferred orders will be much smaller than those seen in the previous quarters.

The education segment continued to suffer from weak demand with procurement orders also not experiencing any rebound in the first quarter of 2022.

First-tier brand vendors are slowing down their order pull-ins in the first quarter of 2022 after the keen shipments in the fourth quarter of 2021. Fewer working hours as a result of the Lunar New Year holidays and power curbs in winter are also expected to undermine their shipments in the first quarter of 2022.

Shipments breakdown

Clients

Chart 3: Shipments by major client, 4Q20-1Q22 (k units)

Source: Digitimes Research, January 2022

Acer was the fifth largest client of Taiwanese notebook makers in the fourth quarter of 2021, taking over Lenovo. Shipments to Fujitsu also surpassed those to NEC in the quarter.

Fujitsu, which focuses mainly on Japan's enterprise segment, saw shipments outperform those of NEC that has a higher proportion of shipments to the consumer segment thanks to an improvement in component supply.

Apple contributed 13% of Taiwan's notebook shipments in the fourth quarter, up 2.2pp sequentially and its highest share ever. In addition to the volume shipments of the US brand's high-end notebooks, orders for Apple's older-generation notebooks targeting the entry-level to mid-range segment also increased more than 10%.

NEC's shipments will surpass Fujitsu in the first quarter of 2022 and NEC will launch its new consumer notebooks, allowing it to suffer from a slower shipment decline than Fujitsu.

HP's gap in terms of shipment share with the second-place Dell will extend to 5.5pp in the first quarter of 2022 as HP still has a large number of deferred enterprise notebook orders from the previous quarter, while brisk orders from Asia's and Europe's enterprise segments will also help offset the declines from the consumer and education sectors.

Chart 4: Shipment share by major client, 4Q20-1Q22

Source: Digitimes Research, January 2022

Chart 5: Global shipments by major vendor, 4Q20-1Q22 (k units)

*Note: Shipments of NEC and Fujitsu-Siemens are included in Lenovo's volumes.

Source: Digitimes Research, January 2022

HP was the largest notebook brand in the fourth quarter of 2021, surpassing Lenovo, as its shipments were significantly increased thanks to an improvement in component supply.

Apple's global share surpassed 10% for the first time in the fourth quarter. Although the vendor's new high-end notebook shipments were undermined by the shortage of backlight modules (BLM), shipments of entry-level and mid-range notebooks still drove up the vendor's shipments in the quarter to near seven million units, the highest record ever.

Huawei's shipments also went up in the fourth quarter as demand for mid-range and high-end models from the China market was up. Huawei also saw its supply of DRAM, which was being banned previously, resumed normal.

HP's shipments will plummet 7% sequentially in the first quarter of 2022 as its shipments of consumer and education models will both slip on quarter, while many orders for enterprise models will remain unsatisfied.

HP's Chromebook shipments may take a nosedive by over 2.5 million units on year, resulting in a drop of 3.2pp in the company's overall notebook shipments share.

Microsoft's shipments of notebooks and tablets were significantly limited by panel and power management IC shortages in the fourth quarter of 2021. With an improvement in component short supply, Microsoft's shipments will rise more than 10% sequentially in the first quarter of 2022.

CPUs

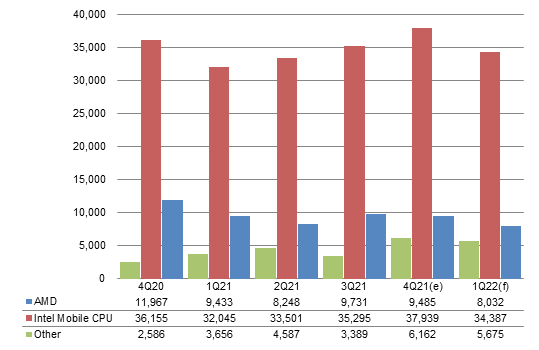

Chart 6: Shipments by CPU, 4Q20-1Q22 (k units)

Source: Digitimes Research, January 2022

Shipments of notebooks powered by Arm-based processors (Other) saw much stronger growth that those of AMD- and Intel-based ones in the fourth quarter of 2021.

The shipment proportion of Arm-based notebooks rose to above 10% in the fourth quarter of 2021 thanks primarily to the contribution from Apple's notebooks equipped with in-house developed M1 processors.

Intel-based notebooks experienced a slower shipment share decline in the fourth quarter of 2021 than AMD-based ones as enterprise models that were the key shipment growth driver were mostly powered by Intel-based CPUs.

The shipment share of Arm-based notebooks will climb further by 0.3pp sequentially in the first quarter of 2022 with that of Intel-based ones also pickup up by 0.7pp to 71.5%.

Apple's high-end notebooks powered by the in-house developed M1 Pro and M1 Max processors are enjoying robust demand in the first quarter, allowing Arm-based notebooks' shipment deceleration to be slower than that of x86-based ones.

Intel-based notebooks' shipment share is expected to increase from a quarter ago in the first quarter of 2022 as Intel's newly released Alder Lake platform is winning orders from brand vendors thanks to their competitive price/performance ratio. AMD raising its CPU prices also pushes consumers to turn to Intel-powered notebooks.

Chart 7: Shipment share by CPU, 4Q20-1Q22

Source: Digitimes Research, January 2022

Screen size

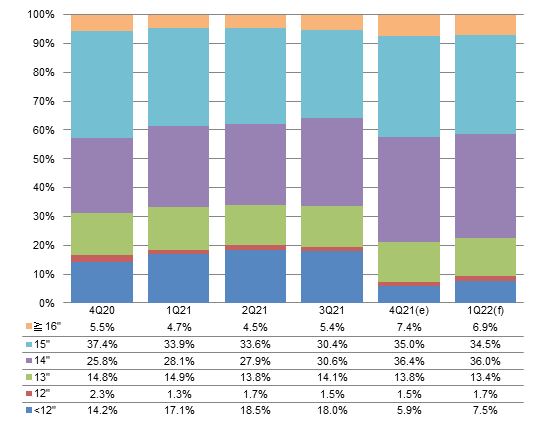

Chart 8: Shipments by screen size, 4Q20-1Q22 (k units)

Source: Digitimes Research, January 2022

Shipments of 14-inch notebooks accounted for the largest share in the fourth quarter of 2021 as the enterprise segment remained the key growth driver for the notebook industry in the second half of 2021.

The proportion of 15-inch notebooks accounted for 35% of Taiwan's overall volumes in the fourth quarter of 2021, up 2.7pp sequentially.

Because of robust demand from the enterprise sector, 14-inch and 15-inch Full HD notebooks had the strongest sales.

Because of a sharp plunge in Chromebook demand, Taiwan's the shipment share of sub-12-inch notebooks slumped 8.9pp sequentially to 5.9% in the fourth quarter of 2021.

Shipment shares of both 14- and 15-inch notebooks are expected to slide from a quarter ago in the first quarter of 2022, while that of sub-12-inch models will rise 1.6pp to come to 7.5%.

The growth in sub-12-inch model's shipment share will be due to Chromebooks having a shipment decline smaller than global average in the first quarter of 2022 plus the fact that Microsoft will begin to partner with brand vendors to promote 11.6-inch education notebooks running Windows 11 SE.

Chart 9: Shipment share by screen size, 4Q20-1Q22

Source: Digitimes Research, January 2022

Makers

Chart 10: Shipments by maker tier, 4Q20-1Q22 (k units)

Source: Digitimes Research, January 2022

Chart 11: Shipment share by maker tier, 4Q20-1Q22

Source: Digitimes Research, January 2022

Chart 12: Top maker shipments, 4Q20-1Q22 (k units)

Source: Digitimes Research, January 2022

Quanta Computer's shipments went up 17.9% sequentially to reach the new highest record ever in the fourth quarter of 2021 thanks primarily to over 10% increases in orders from HP, Asustek and Apple.

Compal Electronics' notebook shipments also hit the highest record ever in the fourth quarter. However, since orders from the company's largest client Dell were flat from a quarter ago in the quarter, Compal had a weaker on-quarter growth than that of Quanta.

Inventec enjoyed increased orders from HP in the fourth quarter, but reduced orders for gaming notebooks from Asustek resulted in a 3.8% sequential decline in overall shipments.

Inventec will only see a 2% sequential drop in first-quarter 2022 shipments as HP's enterprise notebook orders will remain robust, boosting the ODM's shipment share to 10%.

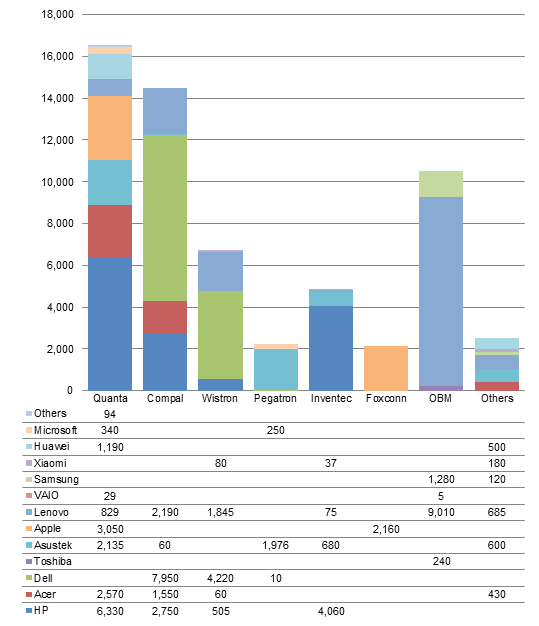

Chart 13: Vendor-maker partnership, 4Q21 (k units)

Source: Digitimes Research, January 2022

Chart 14: Vendor-maker partnership, 3Q21 (k units)

Source: Digitimes Research, January 2022

Chromebooks

Chart 15: Chromebook shipments, 4Q20-1Q22 (k units)

Source: Digitimes Research, January 2022

Chromebook shipments did not rebound as Digitimes Research originally anticipated and went down further by 30.5% sequentially and 60.9% on year to only 4.36 million units in the fourth quarter of 2021.

Despite Google's keen promotions for Chromebooks in the consumer segment and procurement orders from emerging markets, global Chromebook shipments remained in decline in the fourth quarter as procurement orders from major markets had plunged significantly.

HP was the fourth largest Chromebook brand in the fourth quarter of 2021, down from the second place in third-quarter 2021. HP's Chromebook shipments were only 550,000 units in the quarter, down over 700,000 units sequentially as the US-based brand turned its focus to the enterprise segment.

Acer was the largest brand with shipments of 1.1 million units in the quarter as the company has seen more deferred orders than competitors.

Dell shipped 900,000 Chromebooks in the fourth quarter of 2021, while Lenovo shipped 700,000 units, down 500,000 units from a quarter ago as its procurement orders from Japan and the US were both slipped.

Although Chromebooks had traditionally enjoyed sequential increase in the first quarter of a year, the shipments will continue to slip slightly from a quarter ago in the first quarter of 2022 because of feeble demand from the education procurement segment.

Digitimes Research estimates that each brand will only see around 100,000-200,000 units of Chromebook demand a month in the first quarter of 2022.

Important factors

Unsatisfied orders

With most unsatisfied orders being fulfilled in the fourth quarter of 2021 thanks to an improvement in component supply, global notebook shipments hit a new highest record ever in the quarter.

As channels' inventory is returning to the regular level, most brands started cutting their shipment strengthen in the first quarter of 2022, the traditional slow season, in concerns of a potential deceleration in notebook demand.

Issues in China

Although the resurgent of the COVID-19 pandemic in China is growing worse, China's production capability is only seeing limited influences.

Fewer working hours in February as a result of the Lunar New Year holidays and China's power curb are expected to having some minor impact on notebook production.

Components

AMD raised its CPU prices in January as the company is still seeing a shortage of substrates.

Brand vendors have demanded ODMs to prepare several different versions of notebook designs in order for them to switch out components that are in serious shortages with replacement. However, such a strategy is adding up costs for brand vendors and will limit vendors' shipments in the first quarter of 2022.

IC and panel shortages have been improving since the fourth quarter of 2021 and related supply is only expected to be short of demand by less than 5% in the first quarter of 2022 because of seasonality and new 8-inch foundry capacity going online.

Supply of 14- and 15-inch Full HD panels significantly increased since the fourth quarter of 2021 with key suppliers LG Display and AU Optronics (AUO) capable of obtaining sufficient supply of timing controller (T-Con) chips. As a result, shipments of enterprise and mid-range to high-end consumer notebooks performed stronger than expected. Panel supply will further improve in the first quarter of 2022.

Power management ICs from specific integrated device manufacturers (IDM) such as Texas Instruments (TI) are still suffering from more obvious shortages, but brand vendors have started turning to Taiwan-based IC design houses for replacement.

Annual shipments

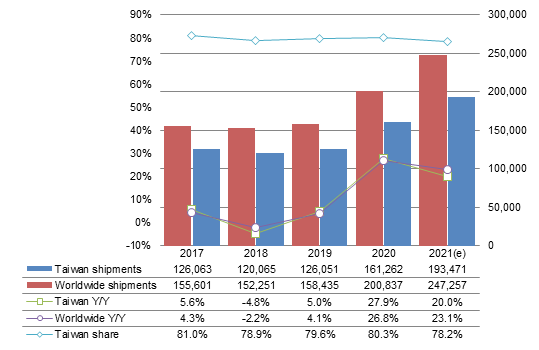

Chart 16: Taiwan and Global notebook shipments, 2017-2021 (k units)

Source: Digitimes Research, January 2022

Chart 17: Top maker shipments, 2018-2021 (k units)

Source: Digitimes Research, January 2022

Chart 18: Global shipments by major vendor, 2018-2021 (k units)

*Note: Starting 2019, Fujitsu-Siemens' shipments are included in Lenovo's volumes as the Chinese brand had completed the acquisition of Fujitsu's PC business.

Source: Digitimes Research, January 2022

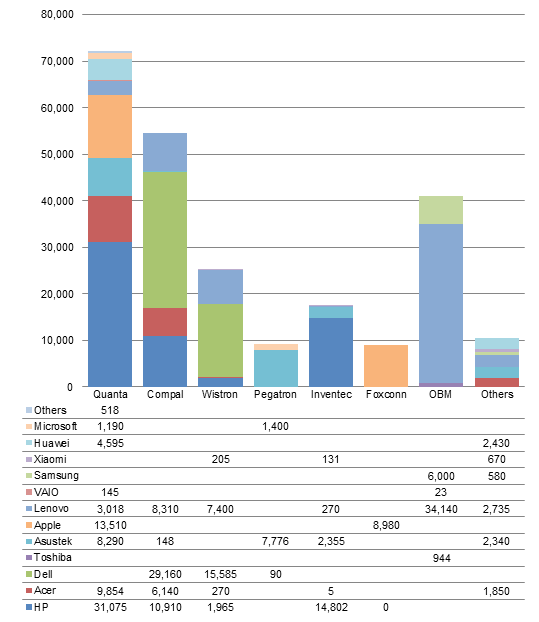

Chart 19: Vendor-maker partnership, 2021 (k units)

Source: Digitimes Research, January 2022